India to Europe air cargo sees unexpected surge in volumes and demand4 Comments19 June 2024

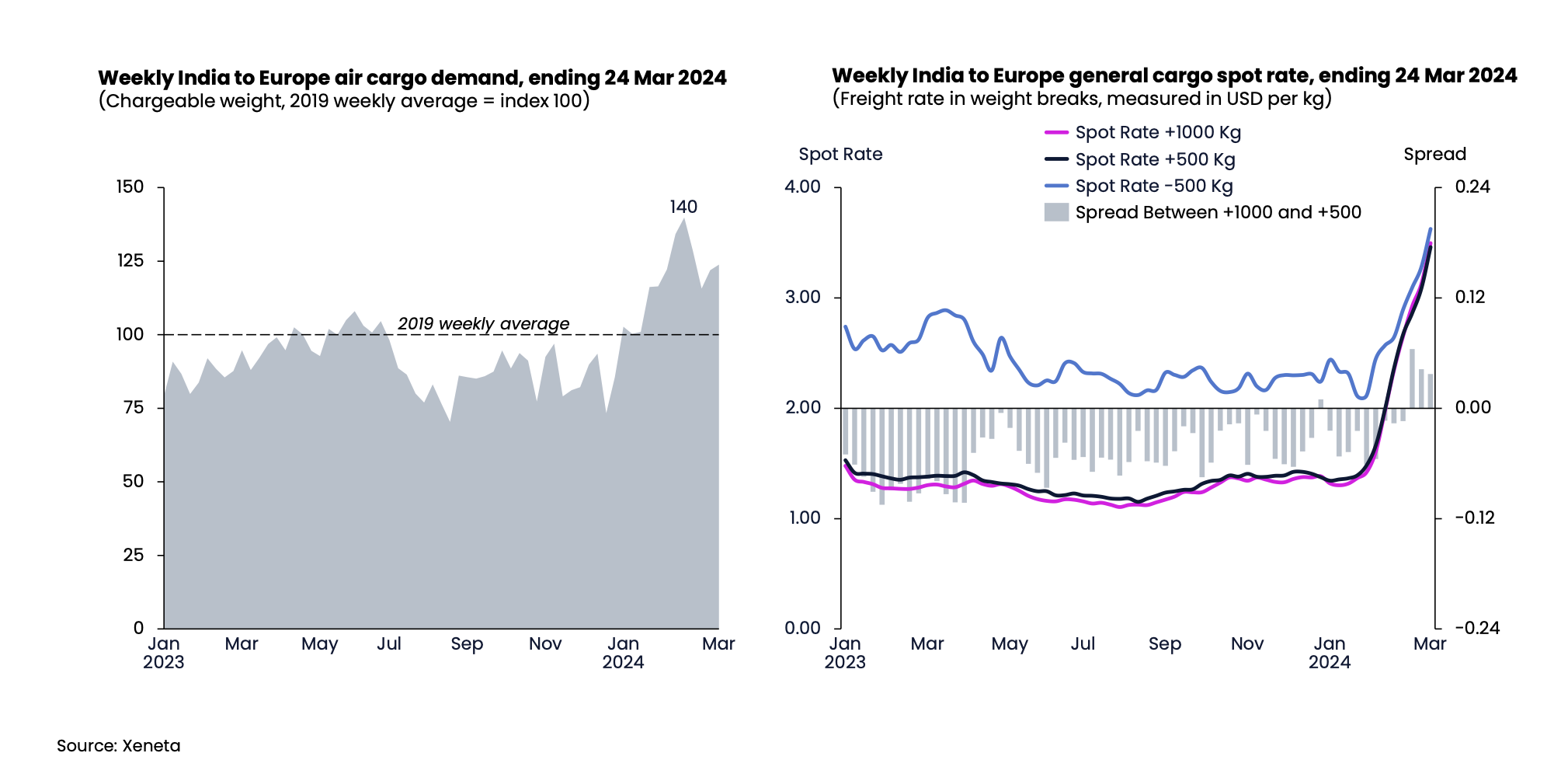

The India to Europe air cargo market has experienced a surge in volumes since the beginning of this year. This has been largely due to demand in apparel exports from India and Sri Lanka coinciding with disruptions to ocean freight services in the Red Sea region, which saw shippers switch transportation mode to air for some of their cargo. These increased general air cargo volumes drove overall air cargo demand in the week ending 25 February to sit 40% higher than the 2019 weekly average. While volumes have dipped slightly since then, in the week ending 24 March they remained 24% above the 2019 weekly average.

With cargo capacity remaining relatively stable, the dynamic load factor from India to Europe climbed to 87% in the week ending 24 March, which is its highest level since April 2022. Xeneta’s dynamic load factor analyzes both the volume and weight of cargo flown alongside available capacity. This increasing load factor has also distorted the usual relationship between weight breaks. Traditionally, larger cargo volumes (more weight) is charged at a cheaper per kg price than smaller volumes (less weight). However, in the week ending 24 March, the general cargo spot rate for +1000 kg reached USD 3.50 per kg, above the spot rate for +500 kg which stood at USD 3.46 per kg. The last time Xeneta observed this market condition was during the onset of the Covid-19 pandemic when the air cargo market encountered a capacity squeeze. A seller’s market India to Europe air freight is a seller’s market at present, which can be seen in the rates sold by airlines (airline-sell). To demonstrate the scale of increase, in the week ending 24 March, the average spot rate stood at USD 3.50 per kg, which is 158% higher than early December before the conflict in the Red Sea. The average airline-sell general air cargo spot rate (valid up to one month) in the week ending 24 March rose above the average seasonal rate by a significant USD 0.86 per kg. This development ended the trend of spot rates sitting below seasonal rates since early May 2022 due to the recovery of cargo capacity in the market. Pushback from shippers As airline-sell rates increased, air shipper rates from India to Europe also faced upward pressure - but not to the same extent. Looking at average short-term rates (valid for no more than three months), the shipper rate for +1000 kg stood at USD 2.56 per kg on 27 March – an increase of 7% compared to three months earlier. However, this 7% increase compares to 152% in the airline-sell rate in the same period. Although shipper rates traditionally respond to airline-sell increases with some delay, the fact we have not seen rates increase to the level we would usually anticipate may be due to pushback from shippers during negotiations with service providers. Red Sea conflict is impacting the market If we want to understand the current movements in the India to Europe air cargo market and how this situation is likely to develop, we should look towards the conflict in the Red Sea region and the impact it has had on ocean freight container services. Ocean containerized spot rates between India and North Europe increased dramatically following the outbreak of conflict in the Red Sea in mid-December last year and reached a crisis peak in early February. Although ocean spot rates have fallen back by around 12% since then, on 27 March they still remained up by 310% compared to their pre-Red Sea crisis level. The slight dip in air cargo demand since the end of February (when it hit 40% above 2019 levels) could be due ocean freight shippers now building longer transit times into their supply chains. In the early days of the crisis some shippers turned to air freight to ensure a steady supply of goods while ocean freight services adjusted to longer sailings around the Cape of Good Hope. While a sense of normality has now returned to ocean freight, the situation is far from fully resolved and we may see some shippers continue to use air freight services for urgent cargo. Given the huge volumes involved in ocean freight shipping, even a small percentage shift in transport mode will likely keep air cargo demand and rates elevated. Underlying demand growth In addition to the switch from ocean to air transport due to the situation in the Red Sea, recent economic indicators may suggest evidence of an underlying demand growth. In February, India’s production growth reached its highest level in five months. In particular, this related to new export orders, with HSBC reporting anecdotal evidence of demand increases from Europe. If so, this could add further upward pressure on the air cargo market. Limited impact of summer schedules Airlines will launch their summer schedules around the Easter holidays in Europe but, unlike other major air corridors, this is unlikely to reduce pressure on the India market. For example, the introduction of summer schedules traditionally sees air cargo capacity increases of over 30% on Transatlantic corridors between the US and Europe. However, the India to Europe trade is less sensitive to this seasonal factor with only single-digit increases in capacity. Therefore, India to Europe air cargo rates are likely to remain elevated in the near term. But, as we have seen in the recent past, ocean and air freight markets can be impacted severely - and rapidly - by major geo-political or environmental incidents. It would be a brave person to bet against further black swan events in 2024, which is why Xeneta customers are continuing to use our data and intelligence platform to monitor both the ocean and air freight markets. This is allowing them to build resilience and agility in supply chains as well as target the lowest rates. By: Wenwen Zhang |

|

{kind=link}

|